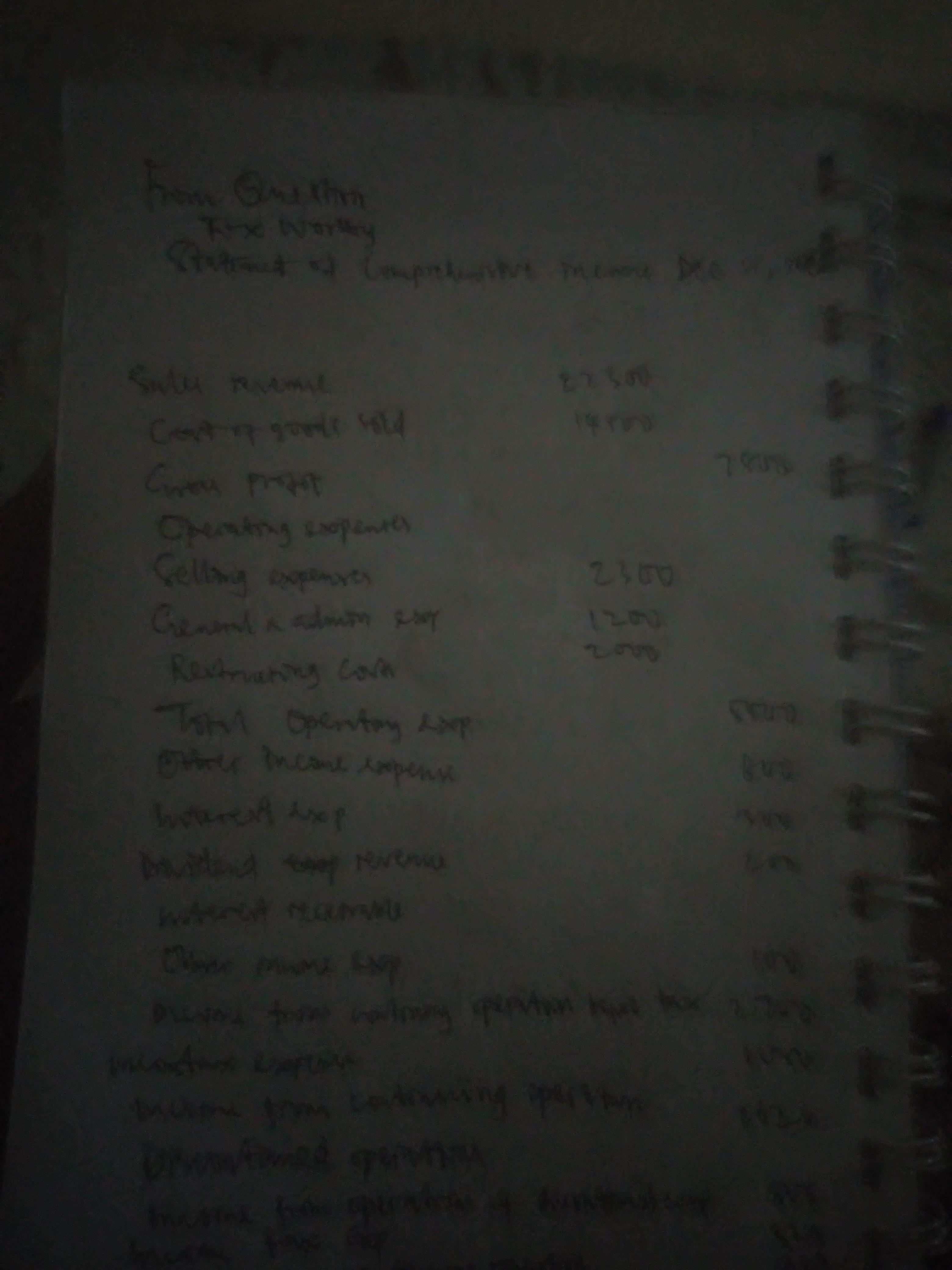

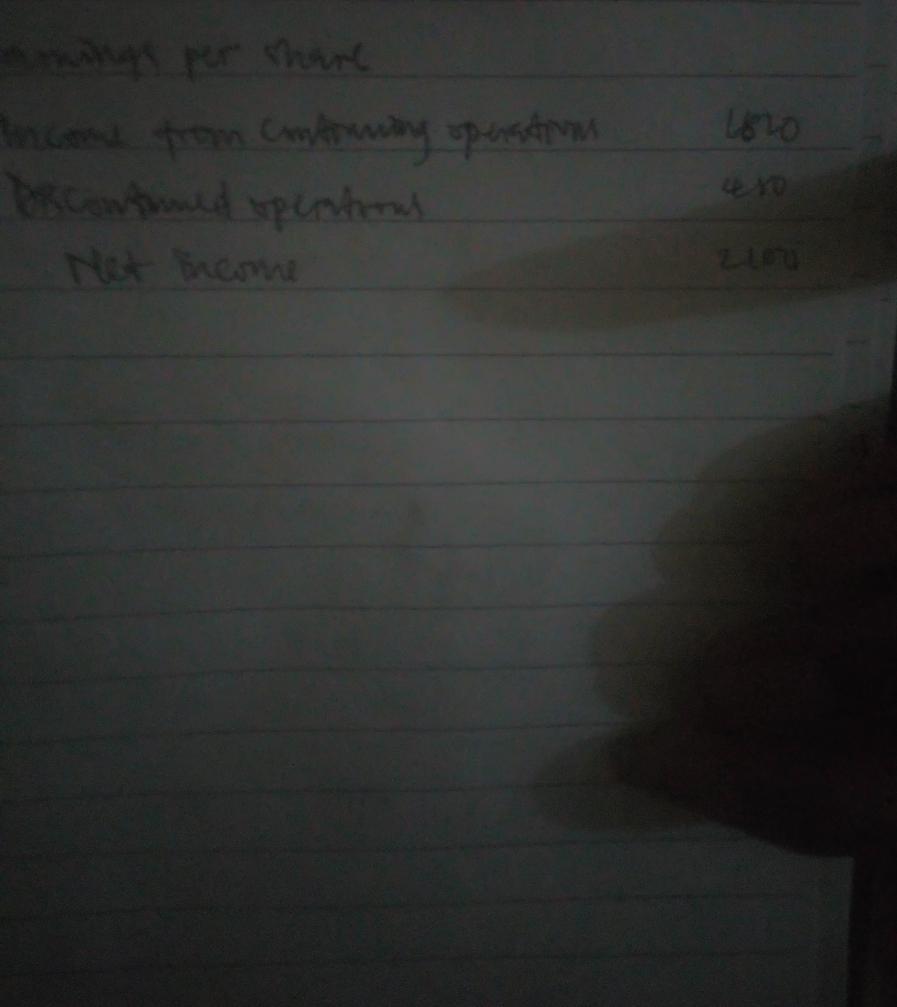

The following income statement items appeared on the adjusted trial balance of Foxworthy Corporation for the year ended December 31, 2021 ($ in 000s): sales revenue, $22,600; cost of goods sold, $14,650; selling expense, $2,330; general and administrative expense, $1,230; dividend revenue from investments, $230; interest expense, $330. Income taxes have not yet been accrued. The company’s income tax rate is 25% on all items of income or loss. These revenue and expense items appear in the company’s income statement every year. The company’s controller, however, has asked for your help in determining the appropriate treatment of the following nonrecurring transactions that also occurred during 2021 ($ in 000s). All transactions are material in amount.

1. Investments were sold during the year at a loss of $300. Foxworthy also had unrealized losses of $200 for the year on investments.

2. One of the company’s factories was closed during the year. Restructuring costs incurred were $2,000.

3. During the year, Foxworthy completed the sale of one of its operating divisions that qualifies as a component of the entity according to GAAP regarding discontinued operations. The division had incurred operating income of $800 in 2016 prior to the sale, and its assets were sold at a

loss of $1,800.

4. Foreign currency translation gains for the year totaled $600.

Required:

Prepare Foxworthy's single, continuous statement of comprehensive income for 2021, including basic earnings per share disclosures. Two million shares of common stock were outstanding throughout the year.

Answers

Question attached

Answer and Explanation:

Please find attached

Related Questions

At a local business school, there is a toasted submarine sandwich process that uses a conveyor-fed oven. ( See picture below) Alice is the sole operator of the sub making process. In the first step of the process, she spends 2 minutes putting various ingredients in the sub. Then, she puts the sub on a conveyor belt and, over a period of 12 minutes, the conveyor moves the sub from the beginning of the oven to the end of the oven, fully toasting it. After the sub comes out of the oven, Alice spends 1 minute slicing the sandwich and putting it in a box. At most, 5 subs can fit in the oven at once. The toasting time in the oven does not depend on the number of subs in the oven.

Required:

a. Draw a process-flow chart for the sandwich-making process.

b. Calculate the hourly capacity of this sandwich-making process.

c. Suppose another employee is hired to do the slicing and boxing, and Zeynep now only loads the sandwiches with the right ingredients. What is the hourly capacity of this process with the additional employee?

Answers

Answer:

b. 20 sandwiches

c. 25 sandwiches

Explanation:

1. I added this diagram of the flow chart as an attachment

2.

Hourly capacity of sandwich making process:

Time it makes to 1 sandwich: 2 + 12 + 1 = 15

The time alice spends when making one sandwich = 2 + 1 = 3

oven uses 12 minutes to process one sandwich, so in 12 minutes, alice can can make 12/3 sandwiches = 4

The Oven can take 5 subs at a time,

So in one hour, the making process

= 60/3 = 20 sandwiches

3.

To calculate Hourly capacity with additional employee:

Alice takes 2 minutes

Additional employees takes 1 minute

Oven uses 12 minutes to make one sandwich

It's only after every 2 minutes Alice can put one sandwich. The oven can take only 5 sandwiches.

So in an hour:

Since oven can take 5

Sandwiches at a time, therefore one sandwich takes,

12 / 5 = 2.4 minutes.

In 1 hour number we have number of processed sandwich as

60 / 2.4 = 25

At hourly capacity with additional employees we have 25 sandwiches

Shenandoah Skies is the name of an oil painting by artist Kara Lee. In each of the following cases, determine the amount and character of the taxpayer’s gain or loss on sale of the painting.

A. The taxpayer is Kara Lee, who sold her painting to the Reller Gallery for $6,000.

B. The taxpayer is the Reller Gallery, who sold the painting purchased from Kara to a regular customer for $10,000.

C. The taxpayer is Lollard Inc., the regular customer that purchased the painting from the Reller Gallery. Lollard displayed the painting in the lobby of its corporate headquarters until it sold Shenandoah Skies to a collector from Dallas. The collector paid $45,000 for the painting.

Answers

Answer:

a. Kara Lee is the painter so the painting is simply part of her normal business operations in selling it.

Amount is $6,000 and this is a sale.

b. Taxpayer is Reller Gallery who sold the painting as part of their normal business operations.

Profit on Sale = Amount sold - Amount purchased

= 10,000 - 6,000

= $4,000

Amount is $4,000 and the nature is ordinary business income.

c. Lollard Inc sold this painting even though it is not part of their normal operations.

This is therefore a gain.

Gain = 45,000 - 10,000

= $35,000

Amount is $35,000 and is a Capital Gain.

A financial instrument just paid the investor $100 last year. If the cash flow is expected to last forever and increase each year at 3%, and with a discount rate of 8%, what should be the price that you are willing to pay for this instrument

Answers

Answer:

Price willing to pay = $2,060

Explanation:

Given:

Cash flow paid = $100

Growth rate (g) = 3% = 0.03

Discount rate (d) = 8% = 0.08

Find:

Price willing to pay

Computation:

Price willing to pay = [(100)(1+0.03)] / [0.08-0.03]

Price willing to pay = 103 / 0.05

Price willing to pay = $2,060

Department Alpha had no beginning inventory. The department added direct materials costing $55,040 and conversion costs of $88,660 during the month of July. Materials are added at the beginning of the process and conversion costs are added evenly throughout the process in this department. During the month, 40,000 units were completed. At the end of July, 3,000 units remained which were 10% complete with respect to conversion costs. What is the correct cost per equivalent unit for materials for July?

Answers

Answer:

Cost per equivalent unit of materials = $1.28

Explanation:

Materials Cost = $55,040

Number of completed units = 40,000

Total units for material = 40,000 + 3,000 = 43,000 units

Cost per equivalent unit of materials = $55,040 / 43,000

Cost per equivalent unit of materials = $1.28

Lina Martinez wants to buy a new high-end audio system for her car. The system is being sold by two dealers in town, both of whom sell the equipment for the same price of $2,000. Lina can buy the equipment from Dealer A, with no money down, by making payments of $118.28 a month for 18 months; she can buy the same equipment from Dealer B by making 36 monthly payments of $70.31 (again, with no money down). Lina is considering purchasing the system from Dealer B because of the lower payment.

Find the APR for Dealer A.

Use the financial calculator and Find the APR for Dealer B

Answers

Answer:

dealer A:

total interest charged = ($118.28 x 18 months) - $2,000 = $129.04

APR = [($129.04 / $2,000) / 1.5 periods] x 100% = 4.3%

dealer B:

total interest charged = ($70.31 x 36 months) - $2,000 = $531.16

APR = [($531.16 / $2,000) / 3 periods] x 100% = 8.85%

The APR charged by dealer A is much lower than the APR charged by dealer B. Even thought the monthly payments are much lower for dealer B, the total amount of interest charged is much higher.

Tom purchased a bond today with a 20-year maturity and a yield to maturity (YTM) of 6%. The coupon rate is 8% and coupons are paid annually. The par value is $1,000. Tom is going to hold this bond for 3 years and sell the bond at the end of year 3. The bond's yield to maturity will change to 8% at the time when Tom sells the bond. Assume coupons can be reinvested in short term securities over the next three years at an annual rate of 10%. Which of the following regarding Tom’s annual holding period return (HPR) of this bond investment is correct?

I. Tom’s annual HPR will be higher than 6% due to a capital gain from selling the bond at year 3

II. Tom’s annual HPR will be lower than 6% due to a capital loss from selling the bond at year 3

III. Tom’s annual HPR will be higher than 6% due to the higher reinvestment rate of 10%

IV. Tom’s annual HPR will be lower than 6% because gains from the 10% reinvestment rate will be largely offset by the capital loss from selling the bond at year 3

a. I only

b. II only

c. III only

d. I and III only

e. II and IV only

Answers

Answer:

The answer happens to be:

e. II and IV only

II. Tom’s annual HPR will be lower than 6% due to a capital loss from selling the bond at year 3

IV. Tom’s annual HPR will be lower than 6% because gains from the 10% reinvestment rate will be largely offset by the capital loss from selling the bond at year 3

Explanation:

An individual has $2000 in physical assets, and $600 in cash initially. This person faces the following loss distribution to the wealth. Full insurance is available at $600

Probability Loss

0.5 0

0.1 200

0.2 400

0.1 1000

0.1 2000

The Individual can also buy partial insurance with i. a $200 deductible, or ii. 75% coinsurance, or iii. Upper limit on coverage, with the limit being $1000. The premium on each partial coverage policy is $450.

Required:

Provide a ranking of the four types of policies for the individual, in terms of preference if the preference function is given by U(FW) = LN(1+FW), where FW is final wealth of the individual.

Answers

Answer with Explanation:

Probability Expected Loss Loss Forecast

0.5 0 0

0.1 200 20

0.2 400 80

0.1 1000 100

0.1 2000 200

1.00 Total 400

Now,

A. Final Wealth with no Insurance = Physical Assets of the person + Cash Assets - Total Loss Forecast

By putting values, we have:

Final Wealth with no Insurance = $2,000 + $600 - $400 = $2,200

B. For Full insurance, we will not consider expected loss because we will receive Insurance Premium instead:

Final Wealth with Full Insurance = Physical Assets + Cash Assets - Insurance Premium

By putting values, we have:

Final Wealth with Full Insurance = $2,000 + $600 - $600 = $2,000

C. Final Wealth with Partial Insurance and $200 deductibles = Physical Assets + Cash Assets - Insurance Premium For Partial Coverage - Deductible

By putting values, we have:

Final Wealth with Partial Insurance and $200 deductibles = $2,000 + $600 - $450 - $200 = $1,950

D. Final Wealth with 75% Co-insurance = Physical Assets + Cash Assets - Insurance Premium - Co-payment

By putting values, we have:

Final Wealth with 75% Co-Insurance = $2,000 + $600 - $450 - (75% * $400)

= $1,850

E. Final Wealth with Partial Insurance and $1,000 Upper Limit = Physical Assets + Cash Assets - Insurance Premium - Maximum Loss Expected

By putting values, we have:

= $2,000 + $600 - $450 - (Probability 0.1 * $2,000) = $1950

From the above, we can say that the best option here in descending order is as under:

1. A. Final Wealth with no Insurance

2. B. With Full insurance

3. C. Final Wealth with Partial Insurance and $200 deductibles & E. Final Wealth with Partial Insurance and $1,000 Upper Limit

4. E. Final Wealth with Partial Insurance and $1,000 Upper Limit

King Costume uses a periodic inventory system. The company started the month with 6 masks in its beginning inventory that cost $8 each. During the month, King Costume purchased 41 additional masks for $10 each. At the end of the month, King counted its inventory and found that 3 masks remained unsold. Using the LIFO method, its cost of goods sold for the month is:

Answers

Answer:

$464

Explanation:

Periodic Inventory method is being used. That means valuation of inventory is done at the end of a specific period.

LIFO method is also used for determining the cost of inventory sold. FIFO stands for Last In First Out.

Calculation of Cost of Goods Sold :

41 unit × $10 = $440

3 units × $8 = $24

Total = $464

The cost of goods sold for the month is: $464

I WILL GIVE BRAINLIEST

Lean and Six Sigma models contradict one another,

True

False

Answers

A company issues $50 million of bonds at par on January 1, 2018. The bonds pay 10% interest semi-annually on 12/31 and 6/30 and mature in 20 years. The journal entry when the bonds are sold is:

Answers

Answer: Please see explanation for answer

Explanation:

Journal entry to record sale of bonds

Account titles Debit Credit

Cash $50,000,000

Bonds Payable $50,000,000

The________ of the message is based on the number of times an average person in the target market is exposed to a message.

Frequency

Quantitative value

Reach

Exposure rate

Answers

The following information about the payroll for the week ended December 30 was obtained from the records of Pharrell Co.:

Salaries:

Sales salaries: $402,000

Warehouse salaries 210,000

Office salaries 165,000

$777,000

Deductions:

Income tax withheld $135,975

Social security tax withheld 46,620

Medicare tax withheld 11,655

Retirement savings 17,094

Group insurance 13,986

$225,330

Tax rates assumed:

Social security 6%

Medicare 1.5%

State unemployment (employer only) 5.4%

Federal unemployment (employer only) 0.6%

Required:

Assuming that the payroll for the last week of the year is to be paid on December 31, journalize the following entries (refer to the Chart of Accounts for exact wording of account titles):

a. December 30, to record the payroll.

b. December 30, to record the employer's payroll taxes on the payroll to be paid on December 31. Of the total payroll for the last week of the year, $40,000 is subject to unemployment compensation taxes.

Answers

Full question attached

Answer and Explanation:

Please find attached

On January 1, 2013, Parent Company purchased 80% of the common stock of Subsidiary Company for $280,000. On this date, Subsidiary had total owners' equity of $250,000 (common stock $20,000; other paid-in capital, $80,000; and retained earnings, $150,000). Any excess of cost over book value is due to the under or overvaluation of certain assets and liabilities. Inventory, which was sold in the third quarter, is undervalued $5,000. Land is undervalued $20,000. Buildings and equipment have a fair value which exceeds book value by $30,000, and a 5-year expected life. Bonds payable are overvalued $10,000. The remaining excess, if any, is due to goodwill. Subsidiary had net income of $60,000 and paid $3,000 in dividends during 2013. Parent had net income of $50,000 and paid $1,000 in dividends during 2013. Assume that Parent uses equity method to record its investment.

Required:

a. Prepare a value analysis schedule for this business combination.

b. Prepare the determination and distribution schedule for this business combination

c. Prepare the necessary elimination entries in general journal form.

Answers

Answer and Explanation:

Please find answer and explanation attached

The company evaluates all projects by applying the IRR Rule. If the appropriate interest rate is 9%, should the company accept this project?

Answers

Answer: The project should be accepted.

Explanation:

The Internal Rate of Revenue is used to evaluate projects before they are accepted. It is a rate that equates the Net Present Value of cashflows to zero.

If the IRR is higher than the Required return then the Project will be accepted because it means that NPV will be higher than zero. The reverse is true.

Given the cashflows in the question, the IRR is;

= 18.8% according to Excel.

With the IRR higher than the required return of 8%, the project should be accepted.

So you want to finance a car for $4,840. Let’s say we offer you a 4.5% interest rate on a 2-year loan and 6% on a 5-year loan. Enter this info into the calculator to see your monthly and total cost by loan term.

Financing Amount

$4840

Correct

Interest Rate on 2-Year Loan

Interest Rate on 5-Year Loan

Answers

Answer:

Interest Rate on 2-Year Loan...$435.6

Interest Rate on 5-Year Loan...$1,452

Explanation:

The formula for calculating simple interest is as follows.

I = P x R x T,

where I = interest

P= Principal

R= interest rate

T= time

For the loan at 4.5 percent for 2 years, the interest will be

= $4,840 x 4.5/100 x 2

= $4,840 x 0.045 x 2

= $435.6

Total cost of the loan will principal plus interest

=$435.6 + $4,840

=$5,275.6

Monthly loan cost

= $5,275.6/24

=$219.81

Total loan cost..$5,275.6

Monthly loan cost ...$219.81

For the Loan at 6 percent for 5 years, the interest will be

= $4,840 x 6/100 x 5

= $4,840 x 0.06 x 5

=$1,452

Total cost of the loan will be principal plus interest

=$ 4,840 + $1,452

=$6,292

Monthly costs will be

=$6,292/60

=$104.87

Total loan cost... $6,292

Monthly loan costs... $104.87

"Ayres Services acquired an asset for $80 million in 2021." The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). Ayers deducted 100% of the asset's cost for income tax reporting in 2021. The enacted tax rate is 25%. Amounts for pretax accounting income, depreciation, and taxable income in 2021, 2022, 2023, and 2024 are as follows: ($ in millions)

2021 2022 2023 2024

Pretax accounting income $330 $350 $365 $400

Depreciation on the income statement 20 20 20 20

Depreciation on the tax return (80 ) (0 ) (0 ) (0 )

Taxable income $270 $370 $385 $420

For December 31 of each year, determine:

a. The cumulative temporary book-tax difference for the depreciable asset.

b. The balance to be reported in the deferred tax liability account.

Answers

Answer:

a. The cumulative temporary book-tax difference for the depreciable asset are as follows:

December 31, 2021 = $60 million

December 31, 2022 = $40 million

December 31, 2023 = $20 million

December 31, 2024 = $0

b. The balance to be reported in the deferred tax liability account are as follows.

December 31, 2021 = $15 million

December 31, 2022 = $10 million

December 31, 2023 = $5 million

December 31, 2024 = $0

Explanation:

Note: See the attached excel file for the calculation of cumulative temporary book-tax difference for the depreciable asset and the balance to be reported in the deferred tax liability account for December 31 of years 2021, 2022, 2023 and 2024 in bold red color.

In the attached excel file, the following formula are used:

Cumulative Temporary differences at December 31 of the current year = Cumulative Temporary differences at December 31 of the previous year + (Depreciation on the tax return at December 31 of the current year - Depreciation on the income statement at December 31 of the current year)

Balance to be reported in deferred tax liability account at December 31 of the current year = Cumulative Temporary differences at December 31 of the current year * Tax rate

Federated Fabrications leased a tooling machine on January 1, 2021, for a three-year period ending December 31, 2023. The lease agreement specified annual payments of $48,000 beginning with the first payment at the beginning of the lease, and each December 31 through 2022. The company had the option to purchase the machine on December 30, 2023, for $57,000 when its fair value was expected to be $72,000, a sufficient difference that exercise seems reasonably certain. The machine's estimated useful life was six years with no salvage value. Federated was aware that the lessor’s implicit rate of return was 10%.

Required:

a. Calculate the amount Federated should record as a right-of-use asset and lease liability for this finance lease.

b. Prepare an amortization schedule that describes the pattern of interest expense for Federated over the lease term.

c. Prepare the appropriate entries for Federated from the beginning of the lease through the end of the lease term.

Answers

Answer:

All requirements solved

Explanation:

we can calculate the right of use asset and lease liability by determining the present value of all future cash flows and after calculating present values sum them up

Requirement 1: Right of use asset and lease liability

Present value (year 0) = 48,000 / (1+10%)^0 = 48,000

Present value (year 1) = 48,000 x 1/(1+10%)^1

Present value (year 1) = 48,000 x 0.909 = 43,636

Present value (year 2) = 48,000 x 1/(1+10%)^2

Present value (year 2) = 48,000 x 0.826 = 39,670

Present value (year 3) = 57,000 x 1/(1+10%)^3

Present value (year 3) = 57,000 x 0.751 = 42,825

Total present value = 48,000 + 43,636 + 39,670 + 42,825

Total present value = 174,131

Right of use asset and lease liability = 174,131

Requirement 2: Amortization schedule

Date payments effective interest Decrease Outstanding

10% in balance balance

1/1/21 174,131

1/1/21 48,000 48,000 126,131

12/31/21 48,000 12,613 35,387 90,744

12/31/22 48,000 9.074 38,926 51,818

12/31/23 48,000 5,182 51,818

Requirement 3: Journal entries

Amortization expense = 174,131/6

Amortization expense = 29,022

1/1/21

Dr Righ of use 74,131

Cr Lease payable 74,131

1/1/21

Dr lease payable 48,000

Cr cash 48,000

12/31/21

Dr Lease payable 35,387

Dr Interest expense 12,613

Cr Cash 48,000

12/31/21

Dr Amortization expense 29,022

Cr Right of use 29,022

12/31/22

Dr Lease payable 38,926

Dr Interest expense 9,074

Cr Cash 48,000

12/31/22

Dr Amortization expense 29,022

Cr Right of use 29,022

12/31/23

Dr Lease payable 51,818

Dr Interest expense 5,182

Cr Cash 57,000

12/31/23

Dr Amortization expense 29,022

Cr Right of use 29,022

Entries into T accounts and Trial Balance Connie Young, an architect, opened an office on October 1, 2019. During the month, she completed the following transactions connected with her professional practice:

a. Transferred cash from a personal bank account to an account to be used for the business, $36,000.

b. Paid October rent for office and workroom, $2,400.

c. Purchased used automobile for $32,800, paying $7,800 cash and giving a note payable for the remainder.

d. Purchased office and computer equipment on account, $9,000

e. Paid cash for supplies, $2,150

f. Paid cash for annual insurance policies, $4,000

g. Received cash from a client for plans delivered, $12,200.

h. Paid cash for miscellaneous expenses, $815

i. Paid cash to creditors on account, $4,500

J. Paid $5,000 on note payable.

k. Received an invoice for blueprint service, due in November, $2,890.

L Recorded fees earned on plans delivered, payment to be received in November, 18,300,

m. Paid salary of assistants, $6,450

n. Paid gas, oil, and repairs on an automobile for October, $1,020

Required:

1. Record the above transactions (in chronological order) directly in the following T accounts, without journalizing. Cash; Accounts Receivable; Supplies; Prepaid Insurance Automobiles; Equipment; Accounts Payable; Notes Payable: Connie Young, Capital; Professional Fees; Salary Expense; Blueprint Expense; Rent Expense; Automobile Expense; s Expense. To the left of each amount entered in the accounts, select the appropriate letter to identify the transaction.

2. Determine the account balances of the T accounts. Accounts containing a single entry only (such as Prepaid Insurance) do not need a balance.

Answers

Answer:

Cash

debit credit

a. 36,000

b. 2,400

c. 7,800

e. 2,150

f. 4,000

g. 12,200

h. 815

i. 4,500

j. 5,000

m. 6,450

n. 1,020

13,865

Accounts Receivable

debit credit

l. 18,300

Supplies

debit credit

e. 2,150

Prepaid Insurance

debit credit

f. 4,000

Equipment

debit credit

d. 9,000

Automobiles

debit credit

c. 32,800

Accounts Payable

debit credit

d. 9,000

i. 4,500

k. 2,890

7,390

Notes Payable

debit credit

c. 25,000

j. 5,000

20,000

Connie Young, Capital

debit credit

a. 36,000

Professional Fees

debit credit

g. 12,200

l. 18,300

30,500

Salary Expense

debit credit

m. 6,450

Blueprint Expense

debit credit

k. 2,890

Rent Expense

debit credit

b. 2,400

Automobile Expense

debit credit

n. 1,020

Miscellaneous Expense

debit credit

h. 815

1 and 2. Recording the transactions in T-accounts and balancing the T-accounts are as follows:

Cash

Account Titles Debit Credit

a. Connie Young, Capital $36,000

b. Rent Expense $2,400

c. Automobile Cash 7,800

e. Supplies 2,150

f. Prepaid Insurance 4,000

g. Professional Fees 12,200

h. Miscellaneous Expenses 815

i. Accounts Payable 4,500

j. Notes Payable 5,000

m. Salary Expense 6,450

n. Automobile Expense 1,020

Ending balance $14,065

Totals $48,200 $48,200

Accounts Receivable

Account Titles Debit Credit

l. Accounts Receivable $18,300

Supplies

Account Titles Debit Credit

e. Cash $2,150

Prepaid Insurance

Account Titles Debit Credit

f. Cash $4,000

Automobiles

Account Titles Debit Credit

c. Cash $7,800

c. Notes Payable $25,000

Ending balance $32,800

Equipment

Account Titles Debit Credit

d. Accounts Payable $9,000

Accounts Payable

Account Titles Debit Credit

d. Equipment $9,000

i. Cash $4,500

Ending balance $4,500

Notes Payable

Account Titles Debit Credit

c. Automobiles $25,000

j. Cash $5,000

Ending balance $20,000

Connie Young, Capital

Account Titles Debit Credit

a. Cash $36,000

Professional Fees

Account Titles Debit Credit

g. Cash $12,200

l. Accounts Receivable 18,300

Ending balance $30,500

Salary Expense

Account Titles Debit Credit

m. Cash $6,450

Blueprint Expense

Account Titles Debit Credit

k. Accounts Payable $2,890

Rent Expense

Account Titles Debit Credit

b. Cash $2,400

Automobile Expense

Account Titles Debit Credit

n. Cash $1,020

Miscellaneous Expense

Account Titles Debit Credit

h. Cash $815

Data Analysis:

a. Cash $36,000 Connie Young, Capital $36,000

b. Rent Expense $2,400 Cash $2,400

c. Automobile $32,800 Cash $7,800 Notes Payable $25,000

d. Equipment $9,000 Accounts Payable $9,000

e. Supplies $2,150 Cash $2,150

f. Prepaid Insurance $4,000 Cash $4,000

g. Cash $12,200 Professional Fees $12,200

h. Miscellaneous Expenses $815 Cash $815

i. Accounts Payable $4,500 Cash $4,500

j. Notes Payable $5,000 Cash $5,000

k. Blueprint Expense $2,890 Accounts Payable $2,890

l. Accounts Receivable $18,300 Professional Fees $18,300

m. Salary Expense $6,450 Cash $6,450

n. Automobile Expense $1,020 Cash $1,020

Learn more: https://brainly.com/question/17463664

Lina Martinez wants to buy a new high-end audio system for her car. The system is being sold by two dealers in town, both of whom sell the equipment for the same price of $2,000. Lina can buy the equipment from Dealer A, with no money down, by making payments of $118.28 a month for 18 months; she can buy the same equipment from Dealer B by making 36 monthly payments of $70.31 (again, with no money down). Lina is considering purchasing the system from Dealer B because of the lower payment.

Find the APR for Dealer A.

Use the financial calculator and Find the APR for Dealer B

Answers

Answer:

dealer A:

total interest charged = ($118.28 x 18 months) - $2,000 = $129.04

APR = [($129.04 / $2,000) / 1.5 periods] x 100% = 4.3%

dealer B:

total interest charged = ($70.31 x 36 months) - $2,000 = $531.16

APR = [($531.16 / $2,000) / 3 periods] x 100% = 8.85%

The APR charged by dealer A is much lower than the APR charged by dealer B. Even thought the monthly payments are much lower for dealer B, the total amount of interest charged is much higher.

Refer to the accompanying figures. If Mallory and Rick are the only two consumers in this market and the price of soda is $0.75 per can, then what will be the market demand for soda each month?

Answers

Answer:

the market demand is 50

Explanation:

The computation of the market demand for soda is shown below:

As we know that the market demand is the sum of the individual demand total

So in the given case, the market demand would be

= Mallory demand at $0.75 per can + Rick demand at $0.75 per can

= 30 + 20

= 50

Hence, the market demand is 50

Suppose that Brazil imports semiconductors from the United States. The free market price is $23.00 per semiconductor. If the tariff on imports in Brazil is initially 12%, Brazilians pay $_____per semiconductor. One of the accomplishments of the Uruguay Round that took place between 1986 and 1993 was significant across-the-board tariff cuts for industrial countries, as well as many developing countries. Suppose that as a result of the Uruguay Round, Brazil reduces its import tariffs to 6%.

Assuming the price of semiconductors is still $23.00 per semiconductor, consumers now pay the price of $_____per semiconductor. Based on the calculations and the scenarios presented, the Uruguay Round most likely_____in Brazil and______in the United States.

Answers

Answer:

Suppose that Brazil imports semiconductors from the United States. The free market price is $23.00 per semiconductor. If the tariff on imports in Brazil is initially 12%, Brazilians pay $25.76 per semiconductor.

= 23 * ( 1 + 12%) = $25.76

One of the accomplishments of the Uruguay Round that took place between 1986 and 1993 was significant across-the-board tariff cuts for industrial countries, as well as many developing countries.

Suppose that as a result of the Uruguay Round, Brazil reduces its import tariffs to 6%.

Assuming the price of semiconductors is still $23.00 per semiconductor, consumers now pay the price of $24.38 per semiconductor.

= 23 * ( 1 + 6%) = $24.38

Based on the calculations and the scenarios presented, the Uruguay Round most likely hurts Producers in Brazil and benefits producers in the United States.

The Uruguay Round reduced the tariff and made the semiconductor cheaper for Brazilians which means they will now import more. This will benefit producers in the US who will now be able to sell more but will hurt producers in Brazil who will sell less if their prices are higher than $24.38.

Blago Wholesale Company began operations on January 1, 2017, and uses the average cost method in costing its inventory. Management is contemplating a change to the FIFO method in 2018 and is interested in determining how such a change will affect net income. Accordingly, the following information has been developed:

2017 2018

Final inventory:

Average cost $150,000 $255,000

FIFO 160,000 270,000

Condensed income statements for Blago Wholesale appear below:

2017 2018

Sales $1,000,000 $1,200,000

Cost of goods sold 600,000 720,000

Gross profit 400,000 480,000

Selling, general, and administrative 250,000 275,000

Net income $150,000 $205,000

Required:

Based on this information, what would 2018 net income be after the change to the FIFO method?

Answers

Answer:

Blago Wholesale Company

New Net income for 2018 = $220,000

Explanation:

Data and Calculations:

Final inventory: 2017 2018

Average cost $150,000 $255,000

FIFO 160,000 270,000

Difference $10,000 $15,000

2017 2018

Sales $1,000,000 $1,200,000

Cost of goods sold 600,000 720,000

Gross profit 400,000 480,000

Selling, general, and

administrative 250,000 275,000

Net income $150,000 $205,000

2018 Net Income after the change to the FIFO method:

Cost of goods sold (weighted average) 720,000

less adjustment for change of method 15,000

Adjusted cost of goods sold 705,000

Income Statement after the change

Sales $1,200,000

Cost of goods sold 705,000

Gross profit 495,000

Selling, general, and

administrative 275,000

Net income $220,000

The December 31, 2018, balance sheet of Whelan, Inc., showed long-term debt of $1,420,000, $144,000 in the common stock account, and $2,690,000 in the additional paid-in surplus account. The December 31, 2019, balance sheet showed long-term debt of $1,620,000, $154,000 in the common stock account and $2,990,000 in the additional paid-in surplus account. The 2019 income statement showed an interest expense of $96,000 and the company paid out $149,000 in cash dividends during 2019. The firm’s net capital spending for 2019 was $1,000,000, and the firm reduced its net working capital investment by $129,000.

Required:

What was the firm's 2019 operating cash flow, or OCF?

Answers

Answer:

606,000

Explanation:

Operating cash flow (OCF) is a measure of the amount of cash generated by a company's normal business operations. Operating cash flow indicates whether a company can generate sufficient positive cash flow to maintain and grow its operations, otherwise, it may require external financing for capital expansion

Operating Cashflow = Cashflow from assets + Net capital spending + Change in Net working capital

Operating Cashflow =(-265,000) + (1,000,000) + (-129,000)

Operating Cashflow = 606,000

Working

New borrowings = Long term borrowings (2019) - Long term borrowings (2018)

New borrowings = 1,620,000 - 1,420,000

New borrowings = 200,000

Cash flow to creditors = Interest expense - new borrowings

Cash flow to creditors = 96,000 - 200,000

Cash flow to creditors = 104,000

New equity = ((Common stock(2019) + additional paid in surplus(2019)) - (Common stock(2018) + additional paid in surplus(2018))

New equity = ($154,000 + $2,990,000) - ($144,000 + $2,690,000)

New equity = 3,144,000 - 2,834,000

New equity = 310,000

Cashflow to stockholders = Dividend (2019) - new equity

Cashflow to stockholders = 149,000 - 310,000

Cashflow to stockholder = -161,000

Cashflow from assets = Cashflow to creditors + cashflow to stockolders

Cashflow from assets = (-104,000) + ( - 161,000)

Cashflow from assets = -265,000

Help pleaseee!

The members of the Federal Reserve System must hold some of their deposits in cash in their vaults. This represents?

A - discount rates

B - reserved requirements

C - selective credit controls

D - open market operations.

Answers

Answer:

B-reserved requirements

Explanation:

The revenue recognition principle states that: Multiple Choice Revenue should be recognized in the period goods and services are provided. Revenue should be recognized in the period the cash is received. Revenue should be recognized in the balance sheet. Revenue is a component of common stock.

Answers

Answer:

Revenue should be recognized in the period goods and services are provided.

Explanation:

IFRS 15 requires revenue to be recognized when control of goods or services has been made to the customer. Control is when all the risks and benefits associated with the product or service has been transferred to the customer.

Seneff Corporation uses the following activity rates from its activity-based costing system to assign overhead costs to products.

Activity Cost Pools Activity Rate

Setting up batches $38.50 per batch

Processing Customer orders $86.62 per customer order

Assembling products $7.33 per assembly hour

Data concerning the two products appear below:

Product V91 Product V21

Number of batches 83 27

Number of customer orders 74 7

Number of assembly hours 702 321

Required:

How much overhead cost was assigned to product V91 using the activity-based costing system?

Answers

Answer:

Total allocated overhead= $14,751.04

Explanation:

Giving the following information:

Activity Cost Pools Activity Rate

Setting up batches $38.50 per batch

Processing Customer orders $86.62 per customer order

Assembling products $7.33 per assembly hour

Data concerning the two products appear below:

Product V91

Number of batches 83

Number of customer orders 74

Number of assembly hours 702

To allocate overhead, we need to use the following formula:

Allocated MOH= Estimated manufacturing overhead rate* Actual amount of allocation base

Setting up= 38.5*83= 3,195.5

Processing= 86.62*74= 6,409.88

Assembling products= 7.33*702= 5,145.66

Total allocated overhead= $14,751.04

Ballou Corporation declared a cash dividend on December 13, 2018, payable on January 10, 2019. By mistake, the company failed to make a journal entry in December 2018. The effect of this error on the financial statements as of December 31, 2018 were:_____.

a. retained earnings was overstated and liabilities were understated.

b. retained earnings was overstated and cash were understated.

c. retained earnings and liabilities were both understated.

d. retained earnings and liabilities were both overstated.

Answers

Answer:

a. retained earnings was overstated and liabilities were understated.

Explanation:

Since in the cash dividend is declared also the same is not recorded by the company

So this error would impact the two account i.e. retained earnings and the liabilities

In this, the retained earning is overstated and the liabilities were understated

Therefore the correct option is a.

And, the rest of the options are wrong

Glumhoff's Packaging Department had the following information at July 31. All direct materials are added at the end of the conversion process. The units in ending work in process inventory were only 28% of the way through the conversion process.

Physical Units Direct Materials Conversion Costs

Units accounted for:

Completed and transferred out 120,000

Ending work in process, August 31 35,000

Total physical units accounted for: 155,000

Total equivalent units

Required:

Complete the schedule by computing the total equivalent units of direct materials and conversion costs for the month.

Answers

Answer:

Explanation:

The total equivalent units of direct materials and conversion costs for the month has been computed and attached.

Note that the conversion cost for the ending work in process was calculated as:

= $35,000 × 28%

= $35,000 × 0.28

= $9,800

Check the attachment for further analysis.

According to Mintzberg, managers averaged ____ written and _____ verbal contacts per day with most of these activities lasting less than ____ minutes. Group of answer choices

Answers

Answer:

1. 36

2. 16

3. 9

Explanation:

According to Henry Mintzberg, a who is known as a professor of Management of Studies. In his model commonly referred to as organizational configurations framework, he concluded that, managers averaged THIRTY SIX written and SIXTEEN verbal contacts per day with most of these activities lasting less than NINE minutes.

Hence, in this case, the correct answer is 36 : 16 : 9

University Printers has two service departments Maintenance and Personnel and two operating departments Printing and Developing. Management has decided to allocate maintenance costs on the basis of machine-hours in each department and personnel costs on the basis of labor-hours worked by the employees in each.

The following data appear in the company records for the current period:

Maintenance Personnel Printing Developing

Machine-hours ? 455 455 2,590

Labor-hours 315 ? 294 1,491

Department direct cost 11,000 $23,000 $25,000 $23,000

Required: Allocate the service department costs using the reciprocal method. Negative amounts should be indicated by a minus sign. Do not round intermediate calculations.

Answers

Answer:

Machine hour percentages -Allocation of Maintenance Costs

455 + 455 + 2,590 = 3,500 total machine hrs

Personnel = 455 / 3,500 = 13%

Printing = 455 / 3,500 = 13%

Developing = 2,590 / 3,500 = 74%

Labor hr. percentages--Allocation of Personnel costs

315 + 294 + 1,491 = 2,100 total labor hrs.

Maintenance = 315 / 2,100 = 15%

Printing = 294 / 2,100 = 14%

Developing = 1,491 / 2,100 = 71%

Service

Maintenance Personnel Printing Developing

Costs before allocation 11,000 23,000 25,000 23,000

Allocate maintenance costs -11,000 1,430 1,430 8,140

0 24,430

Allocate personnel costs 3664.5 -24430 3420.2 17345.3

Allocate maintenance costs -3664.5 476.39 476.39 2711.73

Allocate personnel costs 71.46 -476.39 66.69 338.24

Allocate maintenance costs -71.46 9.29 9.29 52.88

Allocate personnel costs 1.39 -9.29 1.3006 6.5959

Allocate maintenance costs -1.39 0 0 1.39

Total costs 0.00 0.00 30403.87 51596.13

Workings

Allocate maintenance costs

Personnel = (11000 * 13%) = 1430

Printing = (11000 * 13%) = 1430

Developing = (11000 * 74%) = 8140

Allocate personnel costs

Maintenance = 24430 * 15% =

Printing = (24430 * 14%) =

Developing = (24430 * 71%) =

Allocate maintenance costs

Personnel = (3664.5 * 13%)

Printing = (3664.5 * 13%)

Developing = (3664.5 * 74%)

Allocate personnel costs

Maintenance = (476.39 * 15%)

Printing = (476.39 * 14%)

Developing = (476.39 * 71%)

Allocate maintenance costs

Personnel = (71.46 * 13%)

Printing = (71.46 * 13%)

Developing = (71.46 * 74%)

Allocate personnel costs

Maintenance= (9.29 * 15%)

Printing = (9.29 * 14%)

Developing = (9.29 * 71%)